2016 in re-view: graphs and stuff

I’m part way through my analysis of the year and thought I’d just start off with the stuff that is a bit more easy on the eye so here are some graphs with a bit of commentary on each.

If you want a sneak peak at the figures that went into creating these graphs feel free to have a look 1 at the spreadsheet here.

In most cases where it made sense and I have figures for, I’ve added data for the previous year as well (that’s 2015 for those who haven’t been paying attention) to get a nice visual year on year comparison.

Right let’s get going!

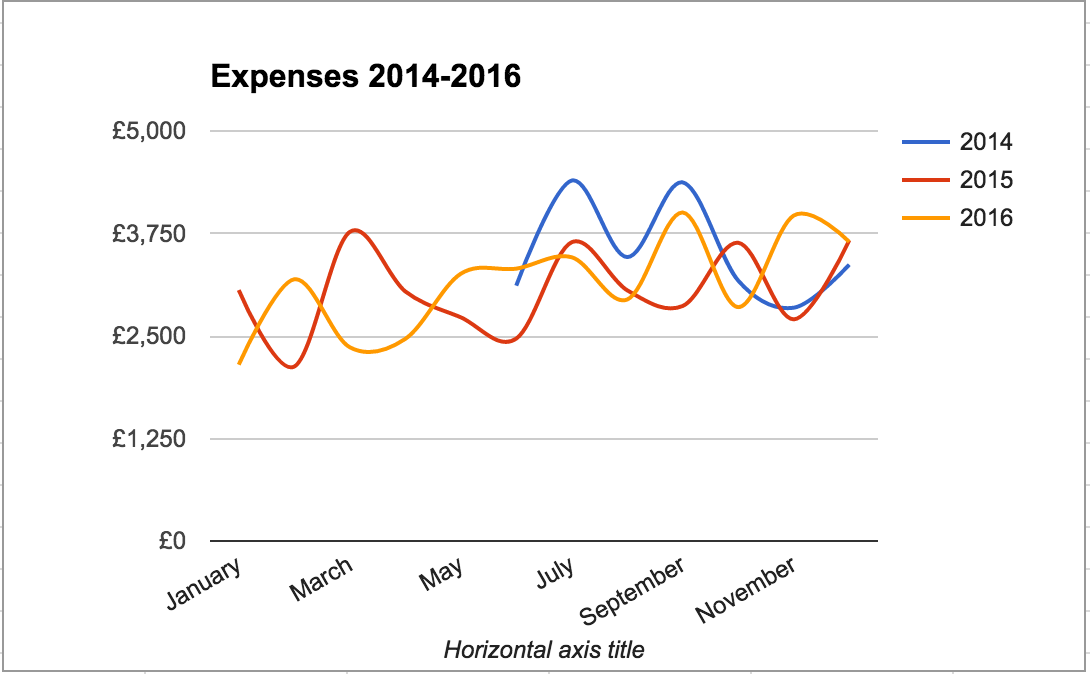

expenses

I think the biggest thing to note here is that the latter months of the year seem to trend much higher than the start months. So maybe our £24K spend in the last 7 months of 2014 when I started tracking our expenses properly wasn’t actually so bad after all. To back that up look at the actual figures:

| Expenses | 2014 | 2015 | 2016 |

| Total | £24,735 | £36,769 | £37,629 |

| Last 7 Months | £24,735 | £22,041 | £24,201 |

Although I’m sure we spent more in the first 5 months of 2014 than we did in the next two years, it is clear that a lot of our big expenses 2 come in the latter half of the year and this is something we need to be aware of, plan for, and certainly remember not get too excited about if we’re looking like frugal sages come the end of May.

income

Not much to say here. The obvious big spike mid year is my bonus.

It’s also nice to see that, especially in the first half of the year at least, it is quite hard to tell that I’ve dropped my hours at work by 25%.

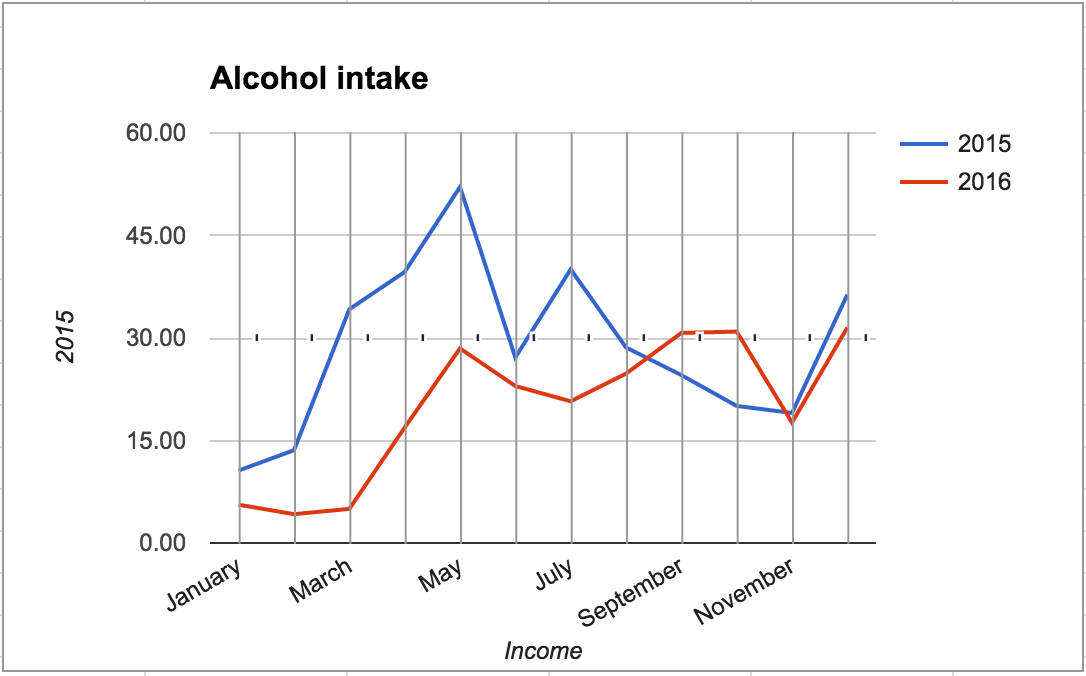

alcohol

What has been tracked must be graphed so here is a nice visual representation of how much I’ve been getting pissed over the last two years 🙂

It’s good to see a clear move in the right direction here.

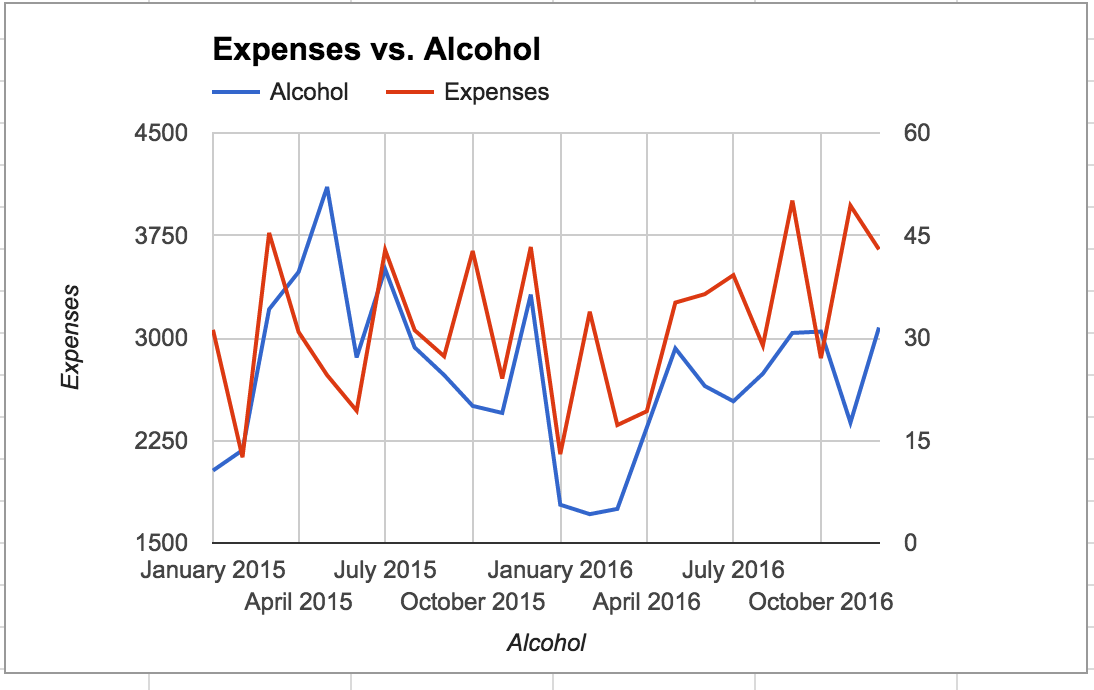

I also had a theory that in the months where we spend more money my alcohol intake is higher, so let’s see how those correlate:

I’d say pretty well!

I’m not saying that drinking causes me to spend more money of course, simply that it normally means we’re out and about more, or are on holiday, and so naturally will end up spending more money as a general rule. An obvious point perhaps but still nice to see it down on the graph. Also I noticed Google Sheets has a really cool feature where you can ask it about the data in your spreadsheets and it will provide you with an answer, such as:

How cool is that!? 🙂

net worth

Here is a graph showing Net Worth, Net Worth excluding housing and Liquid freedom which you could define as anything I can get my hands on before the earliest date I can access my personal pensions (about 57 I believe). I haven’t done this year on year as it makes more sense to just have a separate and continuous line for each.

Well what can I say? A nice steady rise upwards. Obviously it would be nicer if it were a steeper incline but I’m pretty happy with how this graph looks!

savings rate

This correlates with the earlier graph on expenses, with the savings rates dropping off in the latter months of the year.

Obviously the overall savings rates are lower in 2016 which is a shame but the reasons for this are well known by now and I won’t bleat about them again!

death match spending battle

A nice fun one to end on then. You may remember that at the start of last year I reported on our death match spending battle where myself and Mrs T went head to head to see who could spend the lowest amount. She won in 2015!

I am happy to report that I turned the tide and won the 2016 edition!

No one likes a bad winner so I will never mention it again, but here is a graph of both our spendings this year:

As you can see November was inexplicably really expensive for both of us (two holidays I think!?).

The good thing to note is that both of us spent lower than what we did the year before, although I think we were a little slacker on the rules about what counted here. For example in 2015 we counted all upfront holiday costs whereas in 2016 we didn’t count a few flights paid for out of our joint account and stuff like that. It would have seemed a bit harsh to not do this, as our friends sprung on us a Dubai wedding and it would have just totally blown both of our budgets to pay for that out of the “fun money” pot. Having said that, I think next year maybe we should drop the target spending limit again and say all upfront holiday costs (travel and accommodation) are not taken out of these pots. Make the rules a little tighter so to speak and more likely to be consistent from year to year then, despite having more or less expensive travel costs depending on what we end up doing.

coming up…

I’ll go through expenses in a little more detail next time around like last year and forge out a new budget for next year, along with the customary yearly goals review and setting for the up coming year. Last year it all seemed like a bit of a slog and I’m going to try to be much more succinct in my wording, hopefully combining the above into just two more posts.

I’ll finish with some questions as usual…

Do you like my graphs? 🙂

Are there any more data you’d like to see in graphical format?

How did you get on last year? Where do you think we could improve?

Thanks as always for reading!

Headline image copyright of Deadmau5

{kind=link}

{kind=link}

{kind=link}

Discussion (20) ¬

Excellent graphs! It breaks it down to much simpler terms. So far I am collecting data for cash balance net worth and also a separate FIRE portfolio value on a monthly basis. I record the portfolio separately purely as I am interested to try to see its performance compared to benchmarks and see how I am doing purely from the equities bit. I think I will start recording savings rate and try to work out a net worth value this year. I wonder if i should record expenses, as it would probably take slightly more effort and also I don’t really want to be too caught up debating with myself on each and every expense.

What I think would be nice to see is perhaps try put a red line at the target FIRE number in your networth portfolio to give yourself a goal to reach that target for your official FIRE!

All going well for you and the missus tho it seems!

Hi FP,

Glad you like the graphs!

If you record savings rate would you not also have to track expenses by default? You don’t have to get too granular but you at least have to know how much you spent each month.

I agree that debating each and every expense is no way to live but it is good to be aware of how you are spending your cash in case there is any easy fat to trim that is not adding value to your life.

The red line thing is a good idea! I don’t really have a set target right now tbh but could always make one, although it would probably be quite arbitrary.

Cheers!

I currently track my savings by tracking my ‘cash worth’ across all cash accounts monthly. The increase in cash worth is my savings per month. Savings rate would be ‘increase in cash worth’/Net Income… Net income in pretty steady, so any drop in savings would have to do with expenses. I would start looking at expense with theescapeartist’s recent post on how to deal with it. Seems less hassle than recording each and every thing as you go along.

-FIREplanter

Hi FP,

I saw TEA’s post on that but have yet to read it. Will check it out!

I know it’s anal but I do like to keep a track of every last expense, and with Moneydashboard it is actually pretty easy to do this.

I guess I’m just a bit of a control freak at heart… haha.

Also I don’t think the “increase in cash worth’/Net Income” would work for us as out net income seems to be very variable month to month, and also what if I put a chunk into a S&S ISA or a SIPP, then it’s not in cash and my cash worth has gone down. So how can you tell what has happened there?

You can’t (well you can but I don’t think it’s the right way to do it) include SIPP and S&S ISA into cash net worth because the market could add or wipe out far more each month onto your NW than your spending can, so again how would you track that.

Cheers!

Pretty pictures 🙂

Suggestions:

Break your income numbers down into earned (wages, bonus, overtime, commissions), unearned (rent, interest, dividends), and side hustle groupings… a stacked area chart would do the job. Track that over time and as your pile grows you should see the overall proportions slowly tilt away from all earned towards mostly passive. The day it tips over half way is a happy day indeed.

Do a similar income v expenses chart, filtered just for your investment portfolio (including taxes if applicable). If you had an underperforming rental property for example this helps flush out potential holes in your budget… saves you getting in trouble with Mrs TFS for cutting off the Netflix subscription when the real problem was high platform fees or a poor rental yield.

Start tracking the value of your time (income / hours worked+commuting time). It’ll help you figure out when it is time to take a lower paying job closer to home or drop back to working part time. Will also help prioritise/triage the important stuff from the stuff below your noise level.

Hi SD,

I love your first idea! I’ll knock up that chart soon if I can.

The only issue I see here is that I don’t really track my passive income as most of it is in ISA and SIPP so it doesn’t really feel like income just yet as I’m not going to touch it any time soon. Plus some of them are Acc funds not Inc so it is very hard to tell when Divs are paid out in those ones. I guess I could just track the Divs paid out on the Inc ones at the least, and as I add new funds hopefully see this grow, which will be nice.

I agree on the whole income/hours+commuting thing to an extent but my commute allows me to get stuff done – such as writing this comment, for example :). The chances of me getting up early to do blog stuff are pretty much zero, if I worked closer to home but walked or cycled to work.

I know sleep is often underrated but for now I’m happy with the commute, and the reasons I move to a job closer to home will not be down to the (income / hours worked+commuting time) formula but simply because my opinion of it changes, which it is likely to do in about 1 or 2 years I reckon.

It’s definitely something I think about often though, so great advice all the same.

Thanks!

Hi TFS,

I do like a good graph! 🙂 And gives me a great idea as I love the flow showing the expenses over years – I may have to borrow that!

I love the getting p!ssed graph – seems the January hangover kicks in for both drinking and expenses! Glad to see I am not the only one with a graph of NW, NWex. House and Liquid – I also include my original target as well, so I am pushing to get my liquid only over my target line at some point – a seriously tough ask, but one that pushes me!

Afraid you will have to wait for tax year end for my pretty pictures on this lines, but I have a couple of other items that I need to get around to writing!

Cheers,

FiL

Hi FiL,

Glad you liked them and looking forward to seeing your own (and the other posts you have in store) in April

Cheers

Cool graphs, TFS. Fairly weak correlation between alcohol and expenses (and of course correlation is far from the same thing as causation) but a fun idea. Have you done any home brewing recently?

Yes of course, I’m not saying I’m getting drunk then going out making loads of rash purchases like a new Mercedes. But it does show that mainly that when we’re out and about a lot, we’re-a-drinkin’ and we’re-a-spendin’! 🙂

Not since the baby was born! Need to get back on it! 🙂

Love the graphs – the alcohol one looks like some drunk has staggered all over it, haha! Congrats on winning the Death Match Spending Battle!

Haha, I guess that is quite fitting, isn’t it? 🙂

Thanks, but my attention is already on the 2017 re-match… I’ve not started too well put it that way haha.

Love a good graph! I’m liking the juxtaposition of the smooth upward trend of the net worth versus the erratic alcohol graph in particular

Hahah, yes I’d rather it be like that than the other way round 😉

Nice graphs – I love capturing this sort of data I just wish there was an easier way other than fiddling with spreadsheets each month (although I’ll confess to being a bit of a spreadsheet nerd).

One additional graph you could create could be a ‘variable’ expense graph. I consider variable spend to be anything over a month that’s optional. For example, clothes and meals out are probably optional whereas mortgage and council tax isn’t. Although the final graph would mirror your current expenses graph, I think it would more fully show the variance each month, where this is masked slightly by including your mortgage etc at present.

Just a thought!

Cheers,

The Diarist

The Diarist recently posted…My Financial Goals for 2017 (and why I’ll probably fail)

Hi Diarist,

I like your idea! I had kind of a similar view on things when I budgeted last yer with “The boring stuff” (Mortgages etc) and “The fun stuff” (optional spending). So it would be quite easy for me to do this I think and break it down.

I’ll try to remember your idea for next years charts 🙂

Thanks again!