The House Crowd – New website now live!

Welcome to the next instalment of my The House Crowd series. If you missed out on the others see here:

an introduction to The House Crowd

The House Crowd – tax efficient investing

This time round the big news is that The House Crowd have launched their new website! So I thought it would be useful to have a quick look around and see how easy it is to sign up and browse around.

My initial reaction to it was that it seems much easier to navigate and find the information you need, along with the styling update you would expect, which has been jazzed up a bit. I also get the feeling it’s been designed with mobile/tablets in mind because a lot of the buttons are now much bigger and easier to press with sausage fingers, and it also looks responsive i.e. the layout switches automatically when the screen size gets smaller to accommodate those smaller devices, which is great!

the sign up process

This seemed as straight forward as any other website I’ve signed up for. Here is screen one of the sign up process:

This is on the “large mobile view” which I thought I would take screen shots of this view so you could see what was going on a bit better than if I took screen shots of the desktop view which would then be compressed into this tiny space.

Please also note that you shouldn’t use a blatantly fake email address as they email verify you straight after this step 🙂 (sorry to the real Mickey if this caused him to get some unwanted emails!)

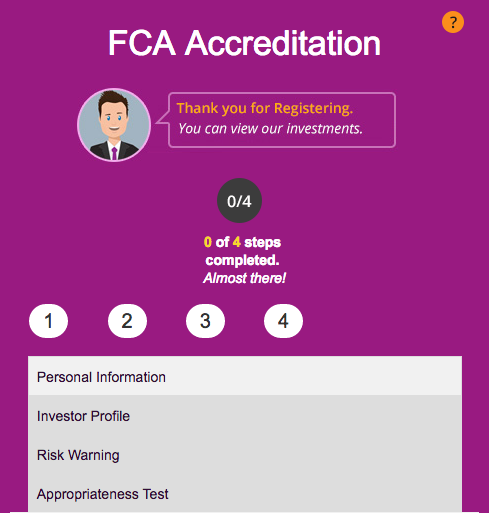

Once your email is verified you need to do a 4 step FCS Accreditation to identify yourself and make sure you understand the risks of investing on such a platform. The four steps are:

- Personal Information (Just confirming your details from earlier, plus occupation)

- Investor profile

- Risk warning

- Appropriateness test

The only 2 really worth talking further about here are 2 and 4.

Pretty simple really, you get to pick what type of investor you are which really boils down to your Net Worth and how much you are planning to chuck at P2P property investments. I’d imagine most people reading would fall under the “Crowdfunding Investor” but if there are any High Net Worth Investors reading please let it be on record that I never said I don’t enjoy a private yacht party or two.

You can also then say what property type and location you are interested investing into. I think I just ticked all the boxes here but this might mean you get a few too many emails from The House Crowd, so you might want to be a bit more choosy than me.

The property type logos, from top left and going clockwise, represent:

- Buy to let

- Short term development

- Commercial

- Leverage investments

- Regeneration

- Tax advantaged investments 1

Appropriateness test

This is probably the hardest part of the sign up process but it’s still very easy and if you get any questions wrong, then in all honesty investing in this sort of thing might not be you in the first place. An example question is here:

And no I’m not going to give you the answers to any of them 😛

That’s it, sign up process done. Now you can browse the site and start investing in properties!

the rest of the site

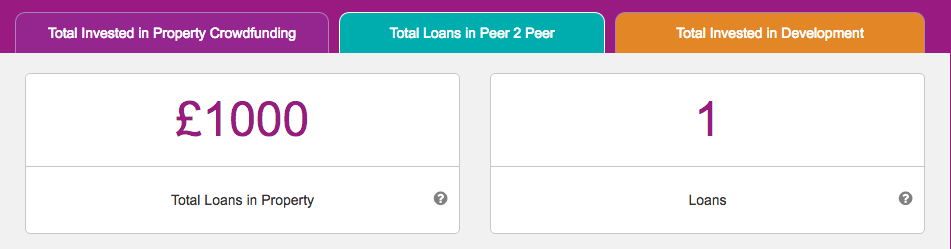

Is actually very straight forward. You can view your personal dashboard to view your current investments, which are split into 3 different tabs to denote the 3 different types of investments available at The House Crowd.

And if you scroll down you can view more details of each investment and download the share certificate:

And view even more details here:

You can obviously also view new properties to invest in, the most important part!

These are handily colour coded by the type of investment – the same colours as the tabs in the dashboard view as you probably have noticed. Examples:

Purple is “Property Crowd funding

Turquoise is “Peer to peer lending”

Yellow is “Property development”

To read more about the differences of each type of investment see either my introduction to The House Crowd or their own crowdfunding information packs here.

If you click on View Details on any of the panels you can get full information on each project including downloadable fact sheets, legal documents, and T&Cs.

Once you are ready to invest you will also need to go through an ID verification process, which is obviously reassuring. To make sure you can jump on a deal you like it might be good to go through this process as soon as you sign up, although in all honesty most properties you will have at least a weeks window if not more to be able to invest after it’s first announced.

All that’s left then is to fund your account, press the button, and The House Crowd will take care of the rest!

wrapping it up

Hopefully that’s given you some insight into the whole investment process at The House Crowd. It’s slightly more long winded than other products I’ve used recently (e.g. Ratesetter) but given the much more complex type of investment, you would expect that. I think they’ve done a good job with the new site of streamlining the process and making it as simple as possible whilst still getting across all the relevant facts and risks inherent in investing in property crowd funding.

Final fun fact, the latest investment opportunity announced is actually in a castle (hence the lead picture above). Yes a full blown freakin’ castle!!! Here it is again for your viewing pleasure 🙂

Notes:

- I notice the designer couldn’t come up with a suitable logo for these last two… a tough ask in all fairness 🙂 ↩

{kind=link}

{kind=link}

{kind=link}

{kind=link}

I’ve read alot about this and also around the concerns of having your money tied up in such an illiquid asset. My understanding is that you can sell your ‘shares’ in the house to other investors however have also heard horror stories of people being stuck with their shares in houses which have lost value or arnt renting out and being unable to exit the market. Whats your thoughts on this?

Hi ERG,

My thoughts are that it is an easier way to get a slice of the BTL et al pie without going the whole hog and buying a property myself. I know I could just go and buy shares in an REIT instead but I like the fact that I can see what properties they are buying and it all seems very transparent to me. I also think that the upside of when they sell a property has much greater potential than you would get with an REIT (obviously the risks are higher to go with that, and liquidity is worse, I am comfortable with that though, I don’t need this money back any time soon).

If you can point to any horror stories of peoples being stuck with shares in houses etc I’d be very interested to hear them? (With THC or any other P2P or similar companies).

Do you have any exposure to property apart from the house you live in (some might say that is way too much already anyway eh 😉 ) and if so where/why/how?

Cheers

Argh! I had written a long post which I’ve now lost, so I’ll just say the short version:

ILLIQUID UNDERLYING + EASE OF INVESTMENT + LOW INTEREST RATES = FLOOD OF CAPITAL = RISK!

This is really high risk stuff IMO. I fully echo EarlyRetirementGuy’s concerns and would make the fundamental point that slicing an illiquid underlying into small, tradeable chunks does not (IMO) make for true liquidity. There won’t be much if any liquidity for any of these investments that go bad.

I don’t doubt the House Crowd’s bona fides (well, only a bit 😉 ) but this is quite dangerous stuff IMV, especially for things like commercial property where you really do need to know what you’re doing.

You may be covering this side of things in future posts but to me, this investment platform really looks quite dangerous.

Sorry to be a party pooper….

Argh, that is so annoying when that happens! I feel your pain 🙂

I don’t think one of the main selling points of THC or any other P2P style property investment platform is that it is liquid and they don’t make a big point of that, and I haven’t even mentioned it in the post above either.

It is very clear that the holding period for most properties will be about 5 years but that if you do need to sell your shares on then there is a possibility of you doing so.

Saying that, there are also short term fixed length loans of 6 months to 1 year available if you don’t want to “buy and hold”, although that’s not liquidity either but at least you “know” you’ll be getting your money back sooner.

If you want true liquidity then stick to trading stocks and shares I guess?

I do want to cover the risks properly in one of these article yes but I have to admit I’m no expert, if you would like to email with more of your thoughts and concerns I would actually be very grateful so drop me a line if you can?

Thanks for your input

Hi TFS,

Apologies for the question but it is a must so when I read your article I have the appropriate context 🙂

Do you have any other type of relation with “The House Crowd” on top of investing through their platform?

Cheers,

Mr Geek

Hi Mr Geek,

A fair question, no worries at all!

I have no relation with them at all other than agreeing to write 12 posts (roughly 1 per month over the course of a year) while they funded a £500 investment for me which is already in my account so I could write about my experiences with the company and investments over the year.

There are no affiliate links on these posts so I have no reason to try to get people to sign up and/or put any positive spin on it other than the already positive opinion I had of the company before they got in touch with me.

Cheers

Interesting stuff, TFS – thanks for posting, I learnt some new stuff there and I’d already signed up to The House Crowd! Alderley Edge is where Premier League footballers and other millionaires live so the price of that development can only go up! That castle looks epic too! That said, THC is currently out of my investment budget range, though I wouldn’t rule out investing in the future. I’m happy to invest smaller amounts at the moment in The Property Moose, which has similar principles and risks. I get where people are coming from about the lack of liquidity but yet so many are happy to get huge mortgages to buy properties… I just think property crowdfunding allows you to dip into such investing without taking on the huge risk of a mortgage etc.

Thanks weenie and glad you found it interesting.

Yea if you compare the risk of getting a BTL mortgage and putting a huge egg into one basket and putting a small percentage of your portfolio into something like THC or Property Moose then it’s clearly less risky doing the latter. Risk isn’t just a probability thing it’s also how bad the outcome might be so with smaller stakes in play, it is inherently less risky. That’s the way I’m looking at it anyway.

Always appreciate the majority of the content you put on your blog, however, I think doing paid articles on stuff like this isn’t helping your cause or the general FI population (especially any one new to FI). Investments like this are unproven and should be viewed as extremely high risk. Just because it’s got a whizz smart easy to use website doesn’t mean the product on offer is sound. £500 commission to write 10 articles about this stuff? You have sold your soul and credidibility far too cheaply sir.

Thanks Mr C for the kinds words at the start but I hope you don’t mind me picking you up on the other points raised…

I think you’ve got this the wrong way round, I was always going to write about THC at some point and they happened to get in touch and offer me the £500 investment to do so. I mean what’s not to like? Admittedly I wouldn’t have written quite so many posts about it but you and anyone else is free to skip them if you don’t find them interesting. See here if you need any more help with that 😉

http://thefirestarter.co.uk/reading-personal-finance-blog-post-dummies/

“You have sold your soul and credidibility(sic) far too cheaply sir.” So you are saying it would have been OK if they were paying me more…? 😉

Also it’s not just about the money, it’s about making contacts, working with the company and so on. Who knows what this might bring in the future. I’m a web developer so if/when I quit my job maybe I can do some contract work for them? These are the sorts of “risks” that are worth taking if you ask me to build connections. Plus I would say I must turn down at least 5 paid post opportunities each week (most I just delete without reading them in fact as you get so many!)

“Investments like this are unproven and should be viewed as extremely high risk” – that’s your opinion and you’re entitled to it, but I respectfully disagree.

“this isn’t helping your cause or the general FI population” – I eagerly await your blog post about the dangers of P2P property investments and other help you have to give the community, feel free to come back and link to it here when it’s up.

Cheers

Hmm, I did a bit of searching and opinions are quite mixed eg. http://moneyweek.com/property-crowdfunding-may-look-tempting-but-its-very-risky/

Personally, I’m rather overexposed to the UK property market already, both residential and commercial, so this isn’t something I’d consider.

Thanks for the link Spreadsheet Man.

I’ll definitely take a look although I’m very wary of anything Moneyweek says because I remember them predicting the end of the World (financially) at least 5 years ago and I think they generally have a very negative/bearish view of things in my very limited experience of reading what they have to say.

Of course if you have lots of property exposure already then any crowdfunding into property is a bit pointless yes 🙂

OK so just read through it. Nothing really new there, yes its a good way of getting into property, but it isn’t without it’s risks. I don’t think anyone ever said it isn’t though (by law they have to say “Capital at risk” about a thousand times on their websites and any advertising by the looks of things) so it should be crystal clear this sort of thing is much riskier than money in the bank. It also mentions liquidity but again these are not sold as particularly liquid investments, although there is a secondary market available with THC (I’ve never tried to buy/sell on it so not sure how that works though).

I would like to cover the risks in the next article as it seems to keep coming up, then it’s done and dusted, so thanks again for the input and link as that has given me some food for thought.

That’s good news and I like the site! I’ll check it out!